Circuit Breakers And Probability Make Our Strategy Possible From A Risk Perspective

Did you know the odds of the Nasdaq falling more than 33% in a single session is basically 0%? The way the system is set up makes it so it is basically impossible. We have something called “circuit breakers”. Anytime the market goes down more than 20% during a given trading day the market stops trading. Now this is based on the S&P 500 but the Nasdaq would not be to far off from that. Why does this matter? It matters because we are trading the TQQQ. The TQQQ is a 3x leveraged Nasdaq 100 ETF. The market (QQQ) would have to fall 33% or more during a single trading session for the TQQQ to blow up and become worthless. It is basically impossible for the Nasdaq to fall more than 33% in a single day due to the circuit breakers and the way the market is set up.

Level 1, S&P 500 drop of 7 percent, trading halt 15 minutes

Level 2, S&P 500 drop of 13 percent, trading halt 15 minutes

Level 3, S&P 500 drop of 20 percent, trading halt the rest of the day

^these make it so the TQQQ can effectively never blow up. I am personally not worried about the TQQQ going to zero because the way the market is set up. We also incorporate puts into our strategies, these help with risk mitigation and can cap losses at a certain percent loss. They also help with portfolio metrics like the Sharpe ration and overall performance and risk.

Lets dive further into the Nasdaq though historically. The worst single day drop for the Nasdaq 100 was March 16, 2020 during Covid. The market dropped 12.6% in a single trading session. TQQQ during that single day lost 34.5%. This would have been mitigated though by our puts. The puts are valuable, they make our strategy competitive and possible. We are able to achieve excess return and great risk metrics due to controlled leverage and options. We also incorporate a moving average crossover strategy to help up time and get a sense of where the market is headed. If you wish to review our strategy and thesis that can be reviewed here: https://www.belvedereinvestmentsco.com/investment-thesis-investment-strategy

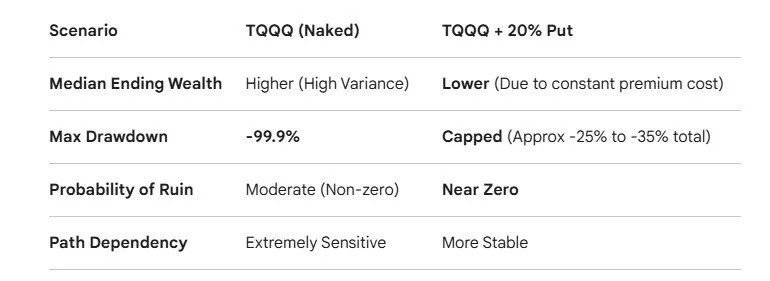

I had AI run a stress test for me based on two scenarios. One with TQQQ naked and one with a 20% downside put. The Monte Carlo simulation said that if we add a put to the strategy (which we already do) the odds of going to zero are near zero. Lets assume zero, other simulations I have done have put the odds of TQQQ blowing up at basically zero percent.